NikkoAM-StraitsTrading Asia ex Japan REIT ETF - SGD Class

ETF

ISIN: SG1DE9000003

Bloomberg Ticker: AXJREIT SP

SGX Code:

CFA (Primary Currency: S$) COI (Secondary Currency: US$)

Intraday NAV*

SGD 0.7877

NAV

as of 17 July 2025

SGD

Total Fund Size

as of 17 July 2025

485470184.11

*The Intraday NAV of the ETF (updated every 15 seconds during the market hours) as shown above (the "data") are provided by

ICE Data Indices, see

ICE Terms of Use, and is updated during SGX trading hours. Powered by

ICE Data Indices, see

Factset.

The Intraday NAV is indicative and for reference purposes only.

@ Refers to all classes of the Fund

*The Intraday NAV of the ETF (updated every 15 seconds during the market hours) as shown above (the "data") are provided by S&P Global and is updated during SGX trading hours. The Intraday NAV is indicative and for reference purposes only.

The investment objective of the Fund is to replicate as closely as possible, before expenses, the performance of the FTSE EPRA Nareit Asia ex Japan REITS 10% Capped Index ("Index"), or upon the Manager giving three (3) months prior written notice to the Trustee and the Holders, such other index that gives, in the opinion of the Manager, the same or substantially similar exposure as the Index.

Fund Details

FTSE EPRA Nareit Asia ex Japan REITs 10% Capped Index

29 March 2017

Open-ended Listed Unit Trust traded on Singapore Exchange

1 unit per lot

Distributions (if any) would be paid quarterly at the Manager’s discretion*

CFA (Primary Currency: S$) COI (Secondary Currency: US$)

* Distributions are not guaranteed and are at the absolute discretion of the Manager.

^ Usual brokerage and handling charges to apply. Please refer to the Fund Prospectus for complete information on the Fund, relevant disclosures and fees payable.

# The total expense ratio will be capped at 0.55% per annum. Any fees and expenses that are payable by the Fund and are in excess of 0.55% per annum of the Deposited Property will be borne by the Manager and not the Fund.

Fund NAV

SGD 0.7877 (17 July 2025)

SGD (17 July 2025)

616,325,000

S$ 1.00

About the Index

What is the FTSE EPRA Nareit Asia ex Japan REITs 10% Capped Index?

FTSE EPRA Nareit Asia ex Japan REITs 10% Capped Index (“the Index”) is a carve out of one of the most widely used global benchmark for listed real estate, the FTSE EPRA Nareit Global Real Estate Index Series.

The Index is a tradable index covering the constituents of developed and emerging countries in the Asia ex Japan region by market capitalisation with a selection process that includes only companies qualified as REITs by international standards and passes certain trading liquidity thresholds. It is designed to represent the performance of qualifying REITS from China, Hong Kong, India, Indonesia, Malaysia, Pakistan, Philippines, Singapore, South Korea, Taiwan and Thailand.

The Index is compiled and calculated by FTSE International Limited using international methodology standards.

How often is the Index rebalanced?

The Index constituents are reviewed on a quarterly basis in March, June, September and December.

For more information on the description of the index methodology and the latest information relating to the Index, please refer to www.ftse.com/products/indices/epra-nareit.

Why FTSE EPRA Nareit Asia ex Japan REITs 10% Capped Index?

1. Exclusive partnership with leading REIT associations

FTSE International Limited, has partnered with European Public Real Estate Association (EPRA) and National Association of Real Estate Investment Trust (NAREIT) to design an Index to provide investors with a comprehensive assessment of listed REIT sector performance across Asia excluding Australia, New Zealand and Japan.

2. Industry leader

The FTSE EPRA/NAREIT Global Real Estate Index Series is a leading global real estate index series with the longest track record, with more than 26 ETFs totalling more than USD10 billion in AUM tracking this series. (Source: FTSE, June 2017)

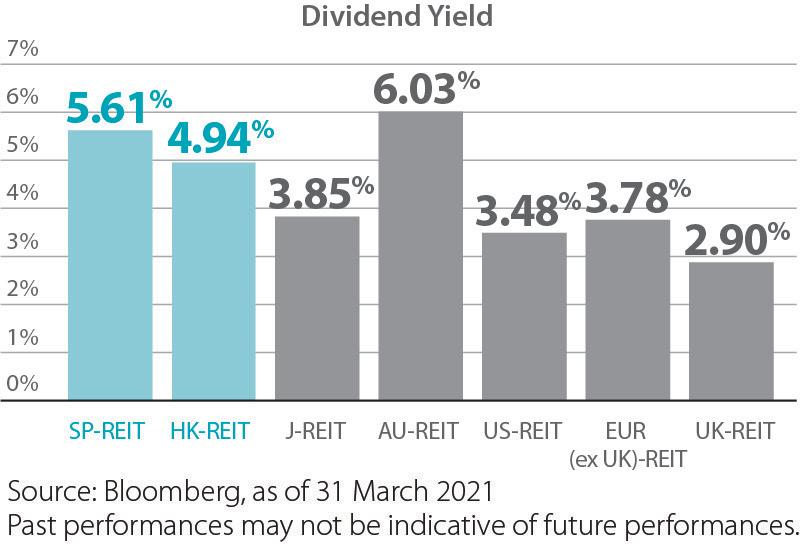

3. Attractive dividend yield

Asia ex Japan REITs offer some of the most attractive dividend yields across the world.

Performance

SGD Class

Return (%)

3 m

6 m

1 yr

3 yr

5 yr

Since Inception

NAV-NAV

2.59

0.99

6.23

-5.01

-1.95

1.44

Benchmark

2.73

1.31

7.09

-4.43

-1.19

2.18

Source: Nikko Asset Management Asia Limited as of 31 May 2025 Returns are calculated on a NAV-NAV basis and assuming all dividends and distributions are reinvested, if any. Returns for period in excess of 1 year are annualised. Past performance is not indicative of future performance.

Fund Characteristics

0.27 %

Source: Nikko Asset Management Asia Limited as of 31 May 2025.

Holdings

Top 10 Holdings

Holdings

Weight

LINK REAL ESTATE INVESTMENT TRUST

11.1 %

CAPITALAND ASCENDAS REIT

10.4 %

CAPITALAND INTEGRATED COMMERCIAL TRUST

10.2 %

EMBASSY OFFICE PARKS REIT

6.7 %

MAPLETREE INDUSTRIAL TRUST

5.1 %

Holdings

Weight

MAPLETREE LOGISTICS TRUST

5.0 %

KEPPEL DC REIT

4.8 %

MAPLETREE PAN ASIA COMMERCIAL TRUST

3.6 %

FRASERS CENTREPOINT TRUST

3.4 %

SUNTEC REAL ESTATE INVESTMENT TRUST

3.2 %

Source: Nikko Asset Management Asia Limited as of 31 May 2025.

Country Allocation (%)

Country Allocation

Country Allocation

Singapore

67.7

Hong Kong

14.1

India

8.5

South Korea

3.5

Malaysia

2.3

Thailand

1.8

Others

1.7

Cash and/or Derivatives

0.4

Source: Nikko Asset Management Asia Limited as of 31 May 2025. Cash in allocation charts includes cash equivalents. Percentages of allocation may not add to 100% due to rounding error.

Sector Allocation (%)

Sector Allocation

Sector Allocation

Retail REITs

32.9

Industrial REITs

27.2

Office REITs

14.7

Diversified REITs

11.9

Data Center REITs

5.5

Hotel & Resort REITs

4.5

Others

2.8

Cash and/or Derivatives

0.4

Source: Nikko Asset Management Asia Limited as of 31 May 2025. Cash in allocation charts includes cash equivalents. Percentages of allocation may not add to 100% due to rounding error.

Tax Transparency

What is the Tax Transparency Treatment?

Tax transparency treatment for REIT ETFs was first announced on 19th February 2018 by the Minister of Finance, Mr. Heng Swee Keat, as part of the tax changes in the 2018 Budget Statement. The change involved extending the tax transparency treatment for Singapore-listed REITs (S-REITs) to Singapore-listed REIT ETFs.

On 9th July 2018, the Inland Revenue Authority of Singapore (IRAS) published the second edition of its e-Tax Guide detailing the income tax treatment of REIT ETFs. Nikko Asset Management Asia Limited, as Manager of the NikkoAM-Straitstrading Asia Ex Japan REIT ETF, applied to be accorded tax transparency treatment status, and was granted the status with effect from 1st July 2018.

The tax transparency treatment states that certain S-REIT distributions will not be taxed in the hands of the trustee of REIT ETF. This is conditional upon the REIT ETF distributing all the distributions it receives from the underlying S-REITs, and that these distributions are made during the period from 1st July 2018 to 31st March 2025.

What does an investor in the NikkoAM-Straitstrading Asia Ex Japan REIT ETF need to do to benefit from the mentioned tax transparency treatment?

1. If you are an Individual Investor

- Holding units in your own name

Distributions made by the ETF to individual unitholders holding units either in their sole names or jointly with other individuals will not be subject to Singapore withholding tax.No further actionis required to benefit from tax transparency treatment.

Backend tax refund – In the case where tax has been over-deducted, you may claim a backend tax refund.

- Holding through a nominee

Tax status declaration will be completed by your Depository Agent. Please liaise with your respective Depository Agent to update your tax status.

Backend tax refund – In the case where tax has been over-deducted, you may claim a backend tax refund through your Depository Agent.

2. If you are a Non-Individual Investor

- Holding units in your own name

Distributions made by the ETF to the followingqualifying unitholdersholding units in their own name will not be subject to Singapore withholding tax:

a) Companies incorporated and tax resident in Singapore

b) Singapore branches of companies incorporated outside Singapore

c) Body of persons (excluding companies or partnerships) incorporated or registered in Singapore, such as: (i) statutory boards; (ii) co-operative societies registered under the Co-operative Societies Act (Cap. 62); (iii) trade unions registered under the Trade Unions Act (Cap. 333); (iv) charities registered under the Charities Act (Cap. 37) or established by any written law; and (v) town councils.

d) International organisations that are exempt from tax on such distributions by reason of an order made under the International Organisations (Immunities and Privileges) Act (Cap.145)

e) Real estate investment trust exchange-traded funds (“REIT ETFs”) which have been accorded the tax transparency treatment.

Furthermore, distributions made by the ETF are subject to a 10% final withholding tax if their distributions are made to qualifyingforeign non-individuals and qualifying foreign funds.

A foreign non-individual investor is one who is not a resident of Singapore for income tax purposes and:

a) who does not have any permanent establishment in Singapore; or

b) who carries on any operation in Singapore through a permanent establishment in Singapore, where the funds used to acquire the units in AXJREIT are not obtained from that operation.

A foreign fund is one who qualifies for tax exemption under section 13CA, 13R or 13X of the Income Tax Act who is not a resident of Singapore for income tax purposes and:

a) who does not have a permanent establishment in Singapore (other than the fund manager in Singapore); or

b) who carries on any operation in Singapore through a permanent establishment in Singapore (other than the fund manager in Singapore), where the funds used to acquire the units in AXJREIT are not obtained from that operation.

You will have to complete a tax status declaration to benefit from tax transparency treatment.

After dividends have been declared for a distribution period, you will receiveForm A(click to download), which is to be completed and returned to Tricor Barbinder Share Registration Services by the stipulated deadline.

Backend tax refund – In the case where tax has been over-deducted, you may claim a backend tax refund.

- Holding through a nominee

Tax status declaration will be completed by your Depository Agent. Please liaise with your respective Depository Agent to update your tax status.

Backend tax refund – In the case where tax has been over-deducted, you may claim a backend tax refund through your Depository Agent.

3. If you are a Depository Agent

Depository Agents holding units as a nominee for unitholders will be required to complete the tax status declaration on behalf of their unitholders. Depository Agents will receiveForm B(click to download), which is to be completed and returned to Tricor Barbinder Share Registration Services by the stipulated deadline.

Reference

The information provided above has been extracted from the IRAS e-TAX Guide – Income Tax Treatment of Real Estate Investment Trust Exchange-Traded Funds and does not constitute as tax advice. For full details, please visit the IRAS website. Readers are advised to seek professional consultation should any clarification be required.

What is the Tax Refund Procedure?

The Manager has established an arrangement with the Inland Revenue Authority of Singapore ("IRAS") to allow eligible NikkoAM-StraitsTrading Asia ex Japan REIT ETF (“AXJREIT ETF”) unitholders to use the back-end tax refund procedures to claim for over-deducted tax on income distributions from the AXJREIT ETF.

Background

Individuals, whether foreign or local, are exempt from tax for distributions made by REITs listed on the Singapore Exchange (“S-REITs”). As such, the portion of distributions made by the AXJREIT ETF that is derived from distributions from S-REITs to the AXJREIT ETF will be tax exempt for individuals holding units of the AXJREIT ETF. Note that individuals who derived the distributions from the carrying on of a trade, business or profession or from a partnership in Singapore are not eligible for this tax exemption and are required to declare the distributions in their income tax returns.

Similarly, qualifying foreign non-individual investors and qualifying foreign funds holding units of the AXJREIT ETF are subject to a reduced rate of tax of 10% for the portion of distributions made by the AXJREIT ETF that is derived from distributions from S-REITs to the AXJREIT ETF.

Accordingly, the Manager of the AXJREIT ETF will determine the income distribution amount to each category of unitholders taking into account the aforementioned tax exemption or reduction.

The aforementioned tax exemption or reduction will take effect from 1 July 2018 to 31 December 2025 (both dates inclusive) (for foreign non-individual investors) and 1 July 2019 to 31 December 2025 (both dates inclusive) (for foreign funds).

In the event where tax has been over-deducted for distributions made to Eligible Unitholders through the AXJREIT ETF, Eligible Unitholders may claim a back-end tax refund.

Unitholders eligible for Tax Refund

Eligible Unitholders are:

1. Foreign Non-individuals holding units in their own name or through Depository Agents; or

2. Foreign funds holding units in their own name or through Depository Agents;

3. Individuals holding units through Depository Agents; or

4. Exempt Non-Corporate Unitholder:

a)A charity registered under the Charities Act (Cap. 37) or established by any written law; or

b)A town council; or

c)A statutory board; or

d)A co-operative society registered under the Co-operative Societies Act (Cap. 62); or

e)A trade union registered under the Trade Unions Act (Cap. 333); or

f)An international organisation that is exempt from tax on such distributions by reason of an order made under the International Organisations (Immunities and Privileges) Act (Cap 145)

Definition of Foreign Non-individual

A foreign non-individual investor is a person (other than an individual) who is not a resident of Singapore* for income tax purposes and:

who does not have a permanent establishment** in Singapore; or

who carries on any operation in Singapore through a permanent establishment** in Singapore, where the funds used to acquire AXJREIT ETF units are not obtained from that operation.

Definition of Foreign Fund

A foreign fund#is one who qualifies for tax exemption under section 13CA, 13X or 13Y of the Income Tax Act, who is not a resident of Singapore* for income tax purposes and;

who does not have a permanent establishment** in Singapore (other than a fund manager in Singapore); or

who carries on any operation in Singapore through a permanent establishment** in Singapore (other than a fund manager in Singapore), where the funds used to acquire the units in AXJREIT are not obtained from that operation.

To make a claim for refund, download the following documents and submit toTricor Barbinder Share Registration Servicesat 80 Robinson Road #11-02, Singapore 068898:

1. Form R1(click to download)For Foreign Non-individualsorExempt Non-CorporateUnitholdersholding units in own name. Complete and submit Form R1, together with Subsidiary Income Tax Certificate ("SITC") or the Annual Dividend Statement ("ADS") issued by the Central Depository (Pte) Ltd (“CDP”) for the distribution in respect of which the refund is claimed.Please use a separate Form R1 for each income distribution period.

ForDepository Agentsfor the benefit of Individuals, Foreign Non-individuals and Exempt Non-Corporate Unitholders holding units through Depository Agent. Particulars of beneficiaries on whose behalf the claim is made must be furnished in the appropriate annexes 1, 2 or 3 to Form R2 and accompanied with Subsidiary Income Tax Certificate ("SITC") issued for the distribution in respect of which the refund is claimed.Please use a separate Form R2 for each income distribution period.

3. ForIndividuals,Foreign Non-individualsor anExempt Non-CorporateUnitholders holding Units through Depository Agents, please liaise with your respective Depository Agent on your claim for the tax refund. The claim will be made on your behalf by your Depository Agent.

When to submit claim

Form R1 and/or Form R2 and accompanying SITC or ADS may be submitted any time toTricor Barbinder Share Registration Services.

The Trustee and the Manager will collate and file a claim for refund to the IRAS on a half-yearly basis (Submission deadline is 30 June and 31 December). For example, all Forms received during the period ending 30 June 2019 will be submitted to IRAS sometime in July/August 2019.

The tax refund will be paid out to eligible investors upon receipt of the tax refund from the IRAS by the Trustee.

Time limit for claim of refund

Every claim of refund must be made to the IRAS within 4 years from the end of the year of assessment to which the claim relates. For example, for claim of refund in respect of distributions made for the period from 1 August 2018 to 31 October 2018, for which distribution payment is some time in February 2019 (which relates to the year of assessment 2020), the claim must be submitted to the IRAS on or before 31 December 2024.

Ways to Invest

REITs Asia ex Japan Market update

Check out our REITs Asia ex Japan Market update video for the latest insights on the REITs market and sector trends.

All you need to know about ETFs

Exchange Traded Funds have grown in popularity, but what exactly is an ETF? What are some of the benefits of ETFs?

What are the different types of ETFs?

Watch this video that breaks it down for you in an easy to understand format.

01 - Trade through your stock broker on the Singapore Exchange (SGX) using:

Cash

CPF

#The Fund is included under the CPFIS - Ordinary Account and has been classified under the category of Higher Risk – Narrowly Focused – Sector – Sector – Others.

Supplementary Retirement Scheme (SRS)

SRS is a voluntary savings scheme to encourage individuals to save for retirement while reducing taxable income.

03 - Direct Subscription through Participating Dealers (for subscriptions of 50,000 units and above)

Subscribe directly to the ETF through any of our participating dealers, subject to minimum unit requirements stated below.

Cash Subscription of New Units

For subscription of new units in the ETF using the cash option, investors need to go through an authorised participating dealer and a minimum of 50,000 units is required.

In-kind Subscription of New Units

For subscription of new units in the ETF using the in-kind option, investors need to go through an authorised participating dealer and a minimum of 500,000 units or multiples of 500,000 is required.

Exchange Traded Funds or “ETFs” are professionally managed investment funds that typically invests in a diversified basket of stocks or bonds that track the performance of a specific index. For example, the Straits Time Index or “STI”[1].

1 The STI tracks the performance of the top 30 companies by market capitalization that are listed on the Singapore Exchange

While most ETFs passively track an index, there are some ETFs that are also actively managed.

Just like stocks, you can trade ETFs on a stock exchange at any point during market hours.

In a nutshell, ETFs offer the best of both worlds, where you have the diversification provided by a fund combined with the tradability of a stock, which can be bought and sold whenever the stock market is open.

For the rest of this FAQ section, unless otherwise specified, the term “ETF” will be used in reference only to passively managed ETFs and not actively managed ones.

How does an ETF work?

As ETFs are designed to track a benchmark index and closely replicate the performance of the index, it will hold substantially all its assets in index securities in the same approximate proportion as their weightings within the index. For example, if DBS represents 20% of the STI, an ETF designed to track the STI would aim to hold 20% of the fund’s assets in DBS shares.

The ETF then issues units to investors, who can buy and sell these units on the stock exchange. The price of an ETF share is determined by the net asset value (NAV) of the underlying assets it holds.

What are the advantages of investing in ETFs?

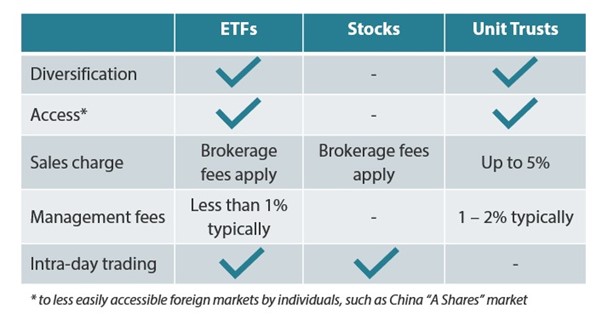

ETFs provide diversification. Investing into an ETF helps you diversify instantly compared to simply buying single stocks. Diversification is important for reducing risk.

ETFs are easy to trade, just like a stock. ETFs trade on the exchange thereby giving you flexibility to enter and exit at any time. Which means you can simply buy and sell an ETF via your broker, subject to prevailing trading liquidity and market prices at any time the stock market is open. Typically, ETFs are supported by market makers to facilitate trading liquidity and tighter bid-ask spreads.

ETFs are also transparent. What you see is what you get. Generally, ETFs are transparent, as the underlying investments in the ETF are disclosed and freely available to the public. This may not always be true in a Unit Trust for example, where the portfolio manager can choose not to reveal all the underlying investments in the fund.

ETFs grant easy and convenient access to a wide variety of markets. Investing directly into some markets, usually emerging markets, may not be easily accessible to the general investing public. ETFs however now make it very easy for investors to conveniently access these traditionally difficult to access markets in bite sized chunks. A very apt example is Nikko AM’s newest NikkoAM-StraitsTrading MSCI China Electric Vehicles and Future Mobility ETF launched in early 2022, that grants investors direct and simple access to China A-shares.

Lower cost, vs other instruments like Unit Trusts. Unlike Unit Trusts that may have higher upfront sales fees and higher management fees to compensate for an actively managed portfolio run by a professional fund manager, passive ETFs typically have lower management fees as they passively track an index to just deliver market returns with no expectations of outperformance.

“Self-Healing”. Constituents within an index are determined by a methodology set by the index provider. New securities are added into the index when they become relevant, and securities that no longer fit the criteria are removed. This ‘self-healing’ nature of the index ensures that the constituents you are invested into via the ETF continues to stay relevant through time, and in turn means that you are always automatically invested into the securities that best fit the index’s objective.

Are ETFs limited to only investing in stocks?

No, ETFs can represent various asset classes, not just stocks. Other asset classes include (but are not limited to) bonds, REITs, commodities etc.

How do I buy or sell ETF units?

As ETF units are traded on stock exchanges, so you can buy or sell them through a brokerage account, just like you would trade individual stocks during trading hours. You place an order with your broker specifying the number of units you want to buy or sell.

What is the difference between ETFs and Unit Trusts?

ETFs and unit trusts are both investment vehicles, but they differ mainly in 2 ways:

The way they are bought and sold – ETFs can be purchased or sold on a stock exchange the same way that a regular stock can, and its price will fluctuate throughout the day. This is different from unit trusts which only trade once a day after the market closes based on its end-of-day net asset value (NAV) price.

ETFs also tend to have lower expense ratios and offer greater transparency.

Do ETFs pay distributions?

Some ETFs pay distributions, especially those that include dividend-paying stocks or income-generating assets like bonds. Distributions are typically made to ETF unit holders on a periodic basis.

Can I reinvest distributions from an ETF?

Yes, brokers may offer distribution reinvestment plans (DRIPs). With a DRIP, you can automatically reinvest your ETF distributions by purchasing additional units, thereby compounding your investment over time.

Are ETFs suitable for long-term investing?

Yes, ETFs can be suitable for long-term investing. They can offer broad market exposure, diversification, and the potential for steady growth. However, it's important to choose ETFs that align with your investment goals and risk tolerance.

Are ETFs risky investments?

As with any investment, there are risks associated with ETFs. As an ETF takes on the risks of the assets it invests into, its net asset value fluctuates with the valuation of these underlying assets, and there is always a possibility of loss. However, ETFs are generally considered to be lower risk compared to individual stocks due to their diversified nature. Do note a passively managed ETF cannot respond to market movements like an actively-managed fund. For example, portfolio manager of an actively-managed fund can adopt defensive measures like reducing securities holdings during periods of volatility or in the face of impending bear market, but a passive ETF will continue to track its index in its securities holdings.

Please note that while this information provides a general understanding of ETFs, it's always important to do thorough research, consult with a financial advisor, and read the specific prospectus and documentation of any ETF you consider investing in.

*The Intraday NAV of the ETF (updated every 15 seconds during the market hours) as shown above (the "data") are provided by ICE Data Indices, see ICE Terms of Use, and is updated during SGX trading hours. Powered by ICE Data Indices, see Factset.

The Intraday NAV is indicative and for reference purposes only.

The Fund is not sponsored, endorsed, sold or marketed by ICE Data Indices, LLC, its affiliates (“ICE Data”) and ICE Data or its respective third party suppliers MAKE NO EXPRESS OR IMPLIED WARRANTIES, AND HEREBY EXPRESSLY DISCLAIM ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE WITH RESPECT TO THE iNAV, IOPV, FUND OR ANY FUND DATA INCLUDED THEREIN. IN NO EVENT SHALL ICE DATA HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, DIRECT, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES. You acknowledge that the data is provided for information only and should not be relied upon for any purpose.

*The Intraday NAV of the ETF (updated every 15 seconds during the market hours) as shown above (the "data") are provided by S&P Global and is updated during SGX trading hours. The Intraday NAV is indicative and for reference purposes only.

The funds mentioned are Singapore registered funds approved for sale or purchase in Singapore. By proceeding, you are representing and warranting that you are either resident in Singapore or the applicable laws and regulations of your jurisdiction allow you to access the information.

This document is purely for informational purposes only with no consideration given to the specific investment objective, financial situation and particular needs of any specific person. It should not be relied upon as financial advice. Any securities mentioned herein are for illustration purposes only and should not be construed as a recommendation for investment. You should seek advice from a financial adviser before making any investment. In the event that you choose not to do so, you should consider whether the investment selected is suitable for you.Investments in funds are not deposits in, obligations of, or guaranteed or insured by Nikko Asset Management Asia Limited (“Nikko AM Asia”).

Past performance or any prediction, projection or forecast is not indicative of future performance. The Fund or any underlying fund may use or invest in financial derivative instruments. The value of units and income from them may fall or rise. Investments in the Fund are subject to investment risks, including the possible loss of principal amount invested. You should read the relevant prospectus (including the risk warnings) and product highlights sheet of the Fund, which are available and may be obtained from appointed distributors of Nikko AM Asia or our website (www.nikkoam.com.sg) before deciding whether to invest in the Fund.

The information contained herein may not be copied, reproduced or redistributed without the express consent of Nikko AM Asia. While reasonable care has been taken to ensure the accuracy of the information as at the date of publication, Nikko AM Asia does not give any warranty or representation, either express or implied, and expressly disclaims liability for any errors or omissions. Information may be subject to change without notice. Nikko AM Asia accepts no liability for any loss, indirect or consequential damages, arising from any use of or reliance on this document. This advertisement has not been reviewed by the Monetary Authority of Singapore.

The performance of the ETF’s price on the Singapore Exchange Securities Trading Limited (“SGX-ST”) may be different from the net asset value per unit of the ETF. The ETF may also be suspended or delisted from the SGX-ST. Listing of the units does not guarantee a liquid market for the units. Investors should note that the ETF differs from a typical unit trust and units may only be created or redeemed directly by a participating dealer in large creation or redemption units.

The Central Provident Fund (“CPF”) Ordinary Account (“OA”) interest rate is the legislated minimum 2.5% per annum, or the 3-month average of major local banks' interest rates, whichever is higher, reviewed quarterly. The interest rate for Special Account (“SA”) is currently 4% per annum or the 12-month average yield of 10-year Singapore Government Securities plus 1%, whichever is higher, reviewed quarterly. Only monies in excess of $20,000 in OA and $40,000 in SA can be invested under the CPF Investment Scheme (“CPFIS”). Please refer to the website of the CPF Board for further information. Investors should note that the applicable interest rates for the CPF accounts and the terms of CPFIS may be varied by the CPF Board from time to time.

The units of NikkoAM-StraitsTrading Asia ex Japan REIT ETF are not in any way sponsored, endorsed, sold or promoted by FTSE International Limited ("FTSE''), by the London Stock Exchange Group companies ("LSEG''), Euronext N.V. ("Euronext"), European Public Real Estate Association ("EPRA"), or the National Association of Real Estate Investment Trusts ("NAREIT") (together the "Licensor Parties") and none of the Licensor Parties make any warranty or representation whatsoever, expressly or impliedly, either as to the results to be obtained from the use of the FTSE EPRA/NAREIT Asia ex Japan Net Total Return REIT Index (the "Index") and/or the figure at which the said Index stands at any particular time on any particular day or otherwise. The Index is compiled and calculated by FTSE. However, none of the Licensor Parties shall be liable (whether in negligence or otherwise) to any person for any error in the Index and none of the Licensor Parties shall be under any obligation to advise any person of any error therein.

"FTSE®" is a trade mark of LSEG, "NAREIT®" is a trade mark of the National Association of Real Estate Investment Trusts and "EPRA®" is a trade mark of EPRA and all are used by FTSE under licence.

Placeholder

Placeholder

Sustainability in action

0.00g

of CO2 is produced loading this sustainable web page.

This site is designed to be light in carbon footprint. We strive to deliver a smoother experience, using less energy with a simplified code, light vector graphics and by reducing unnecessary features and plugins. We regularly review and archive content to reduce impact on the environment.